Commercial Real Estate is a disaster

Soaring office vacancy rates are a much bigger deal than you might think

We have a serious problem.

Not only are people not going back to the office, leases are expiring and companies are not renewing them. This is causing vacancy rates to skyrocket, which means cash flow for building ownership companies is decreasing, which means their entire business model is breaking. Between now and 2025, trillions of dollars of commercial real estate mortgages will have to be refinanced at rates above 10%…and the owners will just hand back the keys. This is a disaster waiting to unfold.

Sibble & Associates provide technical due diligence services to VC firms as well as angel investors, providing clarity and confidence that you are making smart, informed investment decisions.

See, commercial property owners use medium term debt facilities to borrow money to service their commercial mortgages on office buildings on these very expensive properties. Then, they make long term leases and use the cash flow to service this debt and make a profit.

There are two key problems right now though.

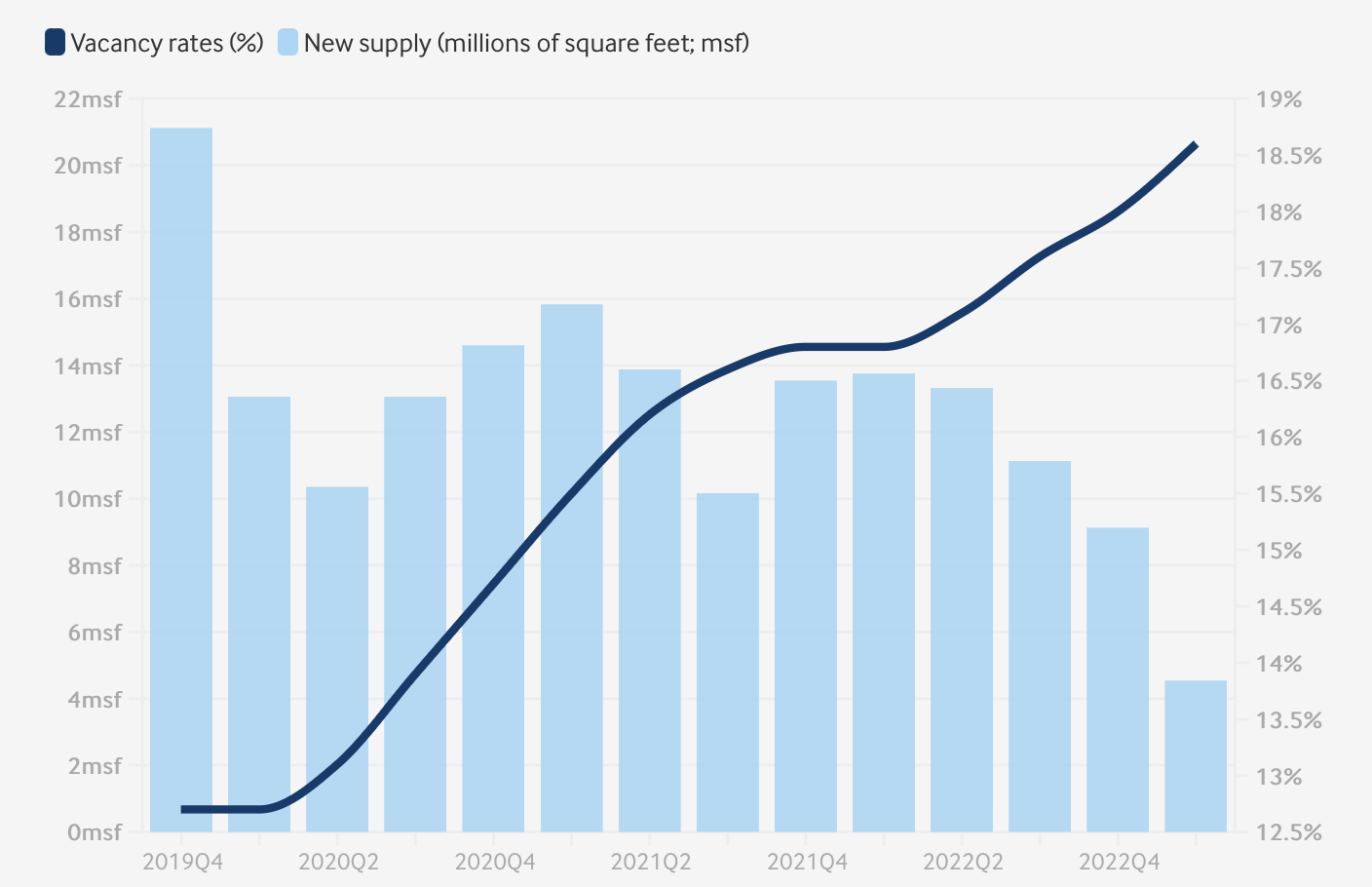

The first is that in order to turn a profit, obviously there need to be tenants occupying above a certain percentage of the building. And quite frankly, we’re below the level that most property companies can make a profit anymore.

And second, these loans are much shorter term than residential 30 year mortgages. They’re usually about five years. Which means the debt needs to be refinanced pretty frequently. And right now, as you probably know, interest rates are very high meaning the cost of that monthly payment for owning the same building skyrockets when the time to refinance comes up. Which would normally mean you’d have to raise prices on your leases, except there’s no demand at current prices.

What all of this leads to is depressed prices in commercial real estate. A building in downtown San Francisco valued at $300 million in 2019 just sold for $65 million or so. That’s a catastrophic destruction of value in only four years.

Now, I’m sure lots of you are thinking, “Haha. Stupid rich landowners getting theirs.”

No. Do not fall into that trap.

This is all of our problems. For two main reasons.

First of all, commercial mortgages are structured as non-recourse loans. That means as long as the bank forecloses on the property, they cannot sue the property owner. And guess what? A lot of building owners have already decided they should just walk away from buildings they are underwater on with no hope of ever turning a profit. Defaults on mortgage payments are going up. Then the bank takes the building, and they are the ones who realize the loss, not the property owners.

And guess what they did? Just like with homes, they’ve securitized these loans and sold them to every investor in the US. So if you own a mutual fund, have a 401k, etc. chances are you own a bunch of this debt. And of course it comes with all the same problems as 2008 like credit default swaps and such.

Except in 2008, all of the problem was caused by about $90 billion in houses defaulting.

The entire commercial office space market is $3.2 trillion. And we’re looking at a decrease in value of 40-80%. That would be marked to market losses of $1.12 to 2.3 trillion.

Quite simply, this is going to make 2008 look like a trial run.

The only good news is anyone anywhere close to commercial real estate sees this coming from a mile away and everyone is setting off the sirens early. Why do you think there are a dozen articles every day saying we all need to get back to work?

The other issues is basically every city in the US gets a large share of its tax revenue from commercial property taxes. I’ve previously written that San Francisco gets somewhere around 40% of its entire tax revenue from this sole source. What are cities going do do when 20-30% of their entire tax revenue just up and disappears? That’s an apocalyptic event. Definitely some cities will fare better than others, but for many it will be a total disaster. Again, some are seeing the writing on the wall and desperately trying to head this off before it happens, as this will take time to unfold, but vacancy rates continue to increase, as employers seem to realize they have lost the WFH fight. Toast just this week paid $16 million to get out of their long term office lease. Good employers know as well as anyone else that work has matured past needing expensive office space. It’s good for employees and it reduces cost for employers. This isn’t going to magically resolve itself as if everyone is suddenly going to decide that going back to soulless open offices was somehow glamorous or remotely enjoyable. Hybrid seems to be the way of the future and that requires a tiny fraction of the space.

So here we are. The people who know this world tell me as property companies have less and less incentive to make their payments, they will continue to walk away from their obligations, and losses in the market will build up. This will be a slow burn, but could be a bad one. Only time will tell.

Author’s Note: I’m copying and pasting a comment on this piece from a friend who works in this industry so you can all see it. He’s even more alarmist than I am.

About $2.5 T of all types of commercial loans will have to refinance between 2024-2025. At more than likely 10%+ interest rate. AND the lenders are going to ask for 50% equity, so more cash at the refi table. Owners will hand back keys.

It’s really, really, really bad.

About $2.5 T of all types of commercial loans will have to refinance between 2024-2025. At more than likely 10%+ interest rate. AND the lenders are going to ask for 50% equity, so more cash at the refi table. Owners will hand back keys.

It’s really , really, really bad.

I foresee the multi-family market in just as bad of situation because of the huge supply from 2020-2023. The rent growth projections used the past three years for these “new construction” deals will fall tremendously short.